Are Youth Sports Worth the Investment? A Financial Perspective for Families

As parents, we can understand the importance of supporting our children’s goals and encouraging them to explore their interests and pursue their dreams. However, as financial advisors, we also understand that sometimes there needs to be a limit to what is allowed.

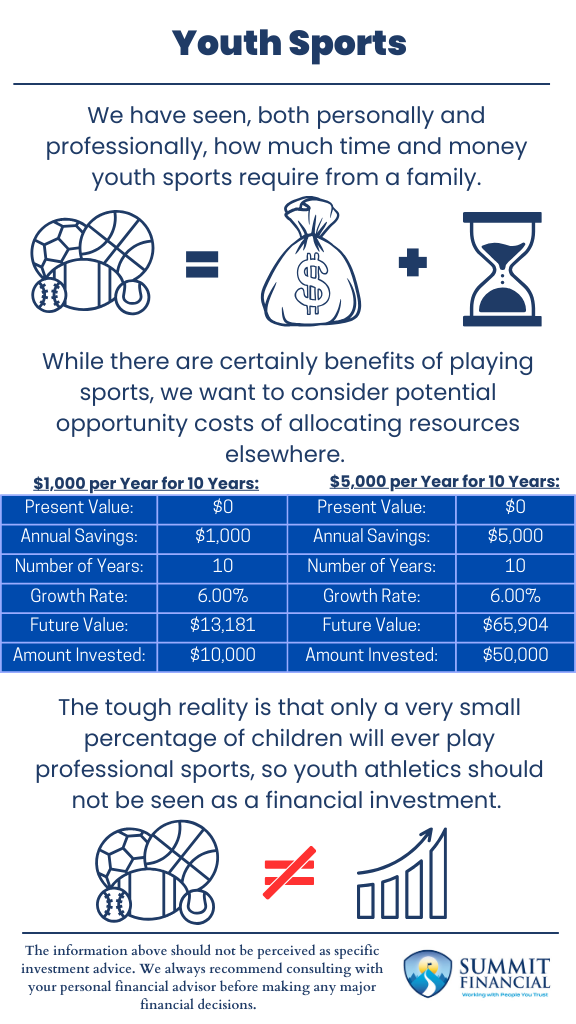

We have seen, both personally and professionally, how much time and/or money youth sports require of a family.

The True Cost of Youth Sports

The overall costs really add up, including registration fees, equipment costs, travel expenses, and possibly even group or private lessons or camps.

One survey states that average cost of youth sports is roughly $700 per year, but we have seen some families spending a lot more than this per year, per child.

For example, another source states that competitive baseball can cost anywhere between $3,000 and $7,000 per year. There is a significant difference in the cost of a child participating in local recreational sports versus playing competitively at a more regional level.

The specific sport also affects the cost to play: ice hockey can average around $2,500 per year, significantly higher than the overall average. We have personally seen families spend over $10,000 per year on competitive hockey or dance.

Benefits of Youth Sports

Now, we definitely agree that there are some benefits to youth sports. A few of these examples are obviously physical health as the kids stay active, improved mental health that typically comes from exercise, and also stronger social skills while playing on a team.

There are also some less well-known additional benefits, such as potentially better academic performance and possibly the opportunity to learn some important life skills.

These benefits may be achievable through other avenues, but sports are certainly a great source to consider. There may be alternative options available to provide some of these benefits at a more cost-effective rate. This is a decision that should probably be made by the parents, based on what they believe is best for their children.

Financial Opportunity Costs of Youth Sports

That said, we want to put these high costs of youth sports in a financial context to illustrate what this total cost could mean over a longer timeframe.

- Example 1:

If a child plays a sport for 10 years and you pay $1,000 per year, then you would have paid a total of $10,000 over that period of time. However, if you were to invest these funds and earn an average of 6% per year, then these funds could have potentially grown to roughly $13,181.

- Example 2:

The numbers are even more drastic if you are paying more for a sport. $5,000 per year is a total of $50,000 paid, and a total of $65,904 after applying that same 6% growth rate.

This is a decent chunk of change that could have been spent elsewhere!

All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or an indication of future results. The information provided is not based on actual current or past clients. All situations are unique, and results will differ depending on individual situation.

The Real Odds of Going Pro

We believe that one reason youth sports may be a high priority for families is that parents (and children) hope their child will end up playing professional sports.

However, that is very unlikely to happen. Even the hope of playing in college can be very high with the intent the child receives some sort of scholarship to help afford the schooling.

Study Example: The Ohio State University did a study and found that:

- Only 6.8% of high school football players ended up playing in the NCAA.

- Only 0.023% of high school football players ended up playing professionally.

These stats can vary by sport and by gender, but we believe the overall concept remains the same.

It is not likely that your child is going to play sports at a high level. In fact, children only spend 3 years on average playing a sport, and most end up quitting by the time they are age 11.

This means that your 8-year-old is not likely to continue playing that same sport (if any) by the time they are in high school — and even if they are, they are still further unlikely to play in college, let alone at a professional level someday.

Other Major Financial Priorities

Do you know what is likely? Your children going to college. In 2019, roughly two-thirds of high school graduates immediately enrolled in college.

This means, financially, that $1,000 or possibly more could have been potentially more useful if the funds were saved and invested inside of an account to help pay for college someday.

- Driving Costs:

It is also very likely that your child will be driving and could use their car by the time they graduate high school. According to a study, almost 60% of 18-year-olds had their driver’s license.

- Other Long-Term Expenses to Plan For:

- Weddings

- Home down payments

- Emergency savings

- Other early-adulthood costs

We have even seen some parents choose to fund their children’s sports rather than setting aside savings for their own retirement plan!

The Hidden Time Costs of Youth Sports

This conversation has not even addressed the time requirement for youth sports.

- Families have to block off time for practices, games, and tournaments.

- Families with multiple children in sports could possibly be busy multiple weeknights and split apart on the weekend trying to divide and conquer the sports obligations.

- Spouses may spend less time together.

- Siblings may not see each other as often.

- Extended family may even fall lower on the totem pole than the athletic commitment.

From experience, we have seen that this large time commitment can be stressful on everyone involved, too, which could cause more tensions among family members.

And while we do not have specific claims or statistics to support this, we personally believe more time spent together as a family could help prevent divorces, which we believe is better for every member of the family.

Final Thoughts: Balancing Financial Wisdom and Family Dreams

Now, do not get us wrong. We still agree that there are certainly benefits from youth sports. However, we want to do our part and ensure our clients understand the financial commitment that is required for the athletic side of childhood.

Ultimately, it is up to the parents to decide:

- How many sports their children will be able to play

- To what extent they are willing to commit

As parents ourselves, we understand it can be very difficult to say no to your children. But as financial advisors, we also know what those funds could grow to and what they could alternatively be spent on in the future.

Are Youth Sports Worth the Cost? Key Takeaways

- We have seen, both personally and professionally, how much time and money youth sports require from a family.

- While there are certainly benefits of playing sports, we want to consider potential opportunity costs of allocating resources elsewhere.

- The tough reality is that only a very small percentage of children will ever play professional sports, so youth athletics should not be seen as a financial investment.

Speak With a Trusted Advisor

If you have any questions about your investment portfolio, retirement planning, tax strategies, our 401(k) recommendation service, or other general questions, please give our office a call at (586) 226-2100. Please feel free to forward this commentary to a friend, family member, or co-worker. If you have had any changes to your income, job, family, health insurance, risk tolerance, or your overall financial situation, please give us a call so we can discuss it.

We hope you learned something today. If you have any feedback or suggestions, we would love to hear them.

Sincerely,

Zachary A. Bachner, CFP®

with contributions from Robert Wink, Kenneth Wink, James Wink

Zach Bachner

After graduating from Central Michigan University in 2017 with specialized degrees in Finance and Personal Financial Planning, Zachary “Zach” Bachner set himself apart by earning the CFP® designation and passing the Series 7, 63, 65 licensing exams early in his career. Zach gained valuable real-world experience with the team at Summit Financial Consulting, who treated him like family. Their guidance helped him refine his skills in practical, client-centered planning, where putting their needs first was non-negotiable. This focus on trust-building not only allowed him to cultivate strong relationships, but also allowed him to continue doing what he loves most: solving client problems through efficient financial planning strategies. Leveraging his experience, Zach now helps others navigate finances through clear, informative writing. His work has been published in major outlets like Yahoo Finance, MarketWatch, and Investment Business Daily, establishing him as a valued resource. By simplifying complex topics, Zach aims to empower everyday people to confidently pursue their financial goals

Sources

- https://ncys.org/the-hidden-costs-of-youth-sports-financial-strain-and-emotional-toll-2/

- https://www.playgroundequipment.com/the-average-cost-of-each-childrens-sport/

- https://www.scripps.org/news\_items/7580-what-are-the-surprising-benefits-of-youth-sports-programs

- https://u.osu.edu/groupbetaengr2367/junran-add-things-here-for-real/#:~:text=After%20simple%20calculation%2C%20we%20can,eager%20for%20a%20professional%20career.

- https://research.com/education/percentage-of-high-school-graduates-that-go-to-college

- https://www.ngpf.org/blog/question-of-the-day/qod-percent-of-16-17-18-year-olds-with-drivers-licenses/