Quantitative Easing vs Quantitative Tightening: Federal Reserve Explained in Plain English

The Federal Reserve's monetary decisions have been a hot topic in recent news coverage, and this has spurred plenty of conversations with our clients. We felt it was appropriate to address the differences between Quantitative Easing and Quantitative Tightening within this blog post.

We have touched on Monetary Policy in the past, and you can review that content for additional background.

One of the goals of the Federal Reserve and other central banks around the world is to implement monetary policy in an effort to maintain a desired balance in their country's economy.

You can think of it as a teeter-totter with Easing policies on one side and Tightening policies on the other.

Their goal is to find a nice balance between the two sides so that the underlying economy can grow at a consistent and sustainable rate. If they ease too much, then the economy might overheat and inflation may rise to an undesired level. If they tighten too much, then the economy might cool down and employment data may suffer as companies struggle to maintain margins.

What is Quantitative Easing?

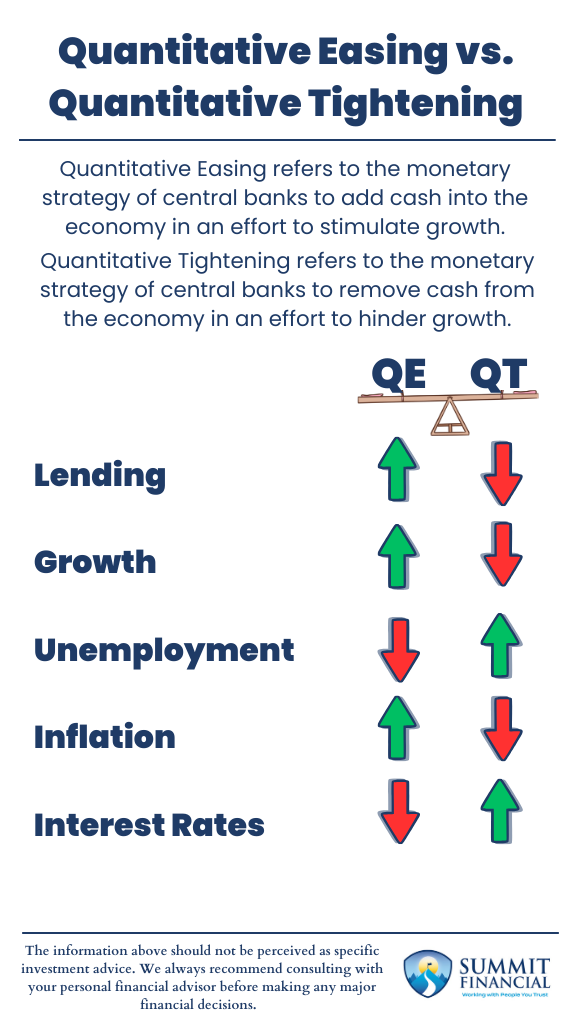

Quantitative Easing refers to the monetary strategy of central banks to add cash into the economy in an effort to stimulate growth. They accomplish this by purchasing assets, such as bonds, from financial institutions.

This allows the government to transfer their cash from the reserves into the hands of the bank, which in turn can then be loaned out to businesses and consumers looking for financing solutions. This can stimulate growth as banks may be more willing to loan out their funds when they have more cash available.

In turn, this could cause interest rates to be lowered as financing becomes more broadly available. Economic growth is normally associated with better employment data but can also be accompanied with higher levels of inflation. More growth can lead to more consumption, which can lead to more demand for goods/services, which can cause prices overall to increase.

If left unchecked, inflation may increase above the desired target levels and thus could hurt the affordability for consumers and businesses. (Source)

What is Quantitative Tightening?

Quantitative Tightening is essentially the opposite strategy of Quantitative Easing with the opposite goals in mind. The Federal Reserve or other central banks will sell assets, or bonds, to financial institutions and thus increase their cash reserves.

The banks will have less cash on hand and may be less willing to lend out the funds they do have. This could cause interest rates to rise, making financing more expensive.

This typically will slow down economic growth as consumers and businesses struggle to find affordable debt funding. In turn, this could cause overall spending to decrease, and unemployment numbers may increase as a result.

Less spending and less consumption should mean less demand for goods/services, and this could cause inflation to decline. The primary concern with this strategy is that if the economy cools too much then it may become difficult for companies to grow or survive and the workforce would likely continue to shrink. (Source)

Impact on Stock and Bond Markets

Both of these strategies can have a direct impact on the stock and bond markets. Bond investments are typically sensitive to interest rate changes while the stock market can be impacted by changes in the underlying economic environment.

The Federal Reserve will be managing these strategies accordingly to keep the economic teeter totter as balanced as they can. They review and interpret various economic reports to ensure they understand where the numbers are currently and can adjust their policy to shift in either direction as needed.

QE vs. QT: Key Takeaways

- Quantitative Easing (QE) adds cash to the economy by purchasing bonds from banks, which can lower interest rates and stimulate economic growth.

- Quantitative Tightening (QT) removes cash from the economy by selling bonds to banks, which can raise interest rates and slow economic growth to control inflation.

Questions About Your Portfolio?

If you have any questions about your investment portfolio, retirement planning, tax strategies, our 401(k) recommendation service, or other general questions, please give our office a call at (586) 226-2100. Please feel free to forward this commentary to a friend, family member, or co-worker.

If you have had any changes to your income, job, family, health insurance, risk tolerance, or your overall financial situation, please give us a call so we can discuss it.

We hope you learned something today. If you have any feedback or suggestions, we would love to hear them.

Best Regards,

Zachary A. Bachner, CFP®

with contributions by Robert L. Wink, Kenneth R. Wink, James D. Wink, and James C. Baldwin

Zach Bachner

After graduating from Central Michigan University in 2017 with specialized degrees in Finance and Personal Financial Planning, Zachary “Zach” Bachner set himself apart by earning the CFP® designation and passing the Series 7, 63, 65 licensing exams early in his career. Zach gained valuable real-world experience with the team at Summit Financial Consulting, who treated him like family. Their guidance helped him refine his skills in practical, client-centered planning, where putting their needs first was non-negotiable. This focus on trust-building not only allowed him to cultivate strong relationships, but also allowed him to continue doing what he loves most: solving client problems through efficient financial planning strategies. Leveraging his experience, Zach now helps others navigate finances through clear, informative writing. His work has been published in major outlets like Yahoo Finance, MarketWatch, and Investment Business Daily, establishing him as a valued resource. By simplifying complex topics, Zach aims to empower everyday people to confidently pursue their financial goals