What Does $39 Trillion in US Debt Mean for Your Portfolio?

One of our main concerns regarding the US economy is actually not the impact of the ongoing war in Iran, nor is it high inflation. We believe one of the biggest hurdles that the US economy is facing, and will continue to increasingly face, is the amount of outstanding debt.

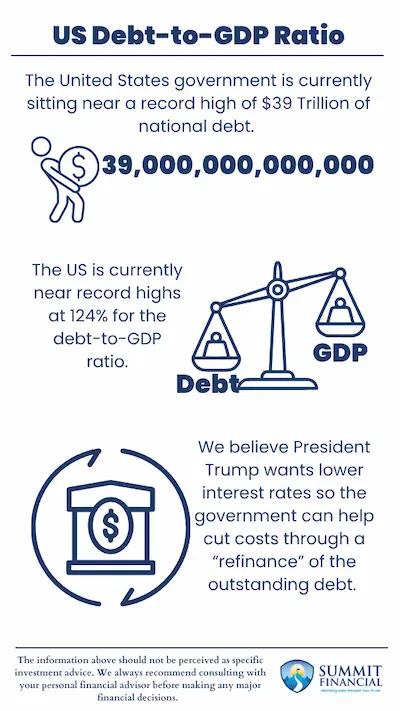

At the time of this writing, the United States currently has over $39,000,000,000,000 in debt. Yes, that is over $39 Trillion! (fiscaldata.treasury.gov)

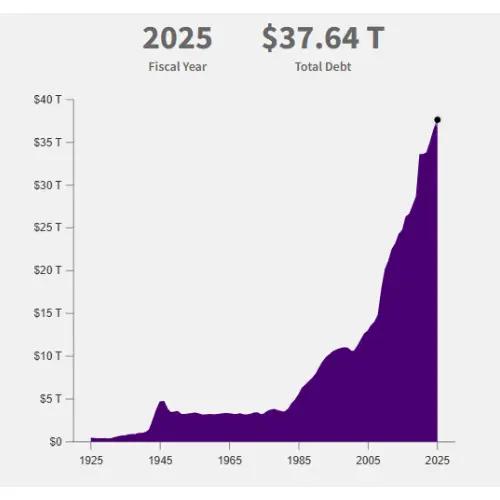

This graphic posted by fiscaldata.treasury.gov shows how quickly the nation's debt has been accelerating. We went from $3.8 Trillion in debt to over $10 Trillion by 2001 and then up to the current $39 Trillion since then. The trend on this graph is very clear and the national debt historically has been skyrocketing over the past few decades.

How Does the Government Continue to Accumulate Debt?

Well, that answer is the same for any business or household too. They spend more than they earn. This means that the US Government has historically been operating under a cash flow deficit and relies on debt issuance to pay for any remaining expenses.

Carrying debt, or leverage, is not inherently a bad thing. But when the debt continues to snowball and those interest payments become larger and larger, this is when the concern sets in that the debt holder may not be able to sustain their minimum payments.

How Can We Understand This Using a Household Analogy?

A more household-oriented illustration might help readers grasp this concern. Let us say that a couple has been approved for a $500,000 mortgage. They decide to buy a home at the very top of what they were approved at, so cash flow is going to be tight.

But upon moving in, they realized they needed to make some important repairs, and they still needed to furnish their new home. They decide to put all of these charges on a credit card.

Their credit card payments are more than they can afford, so they are forced to continue to use their credit cards to pay for their monthly expenses. And after a few months they seem to get things under control, but then their driveway needs an urgent repair, which causes them to take on more credit card debt.

After living in the home for awhile, they cannot seem to avoid turning to their credit cards and their debt continues to increase and increase, which may lead to bankruptcy or even foreclosure on their home.

Obviously, this is not a great picture, but this is similar to the concerns regarding the nation's outstanding debt. The government is operating at a deficit, so they already cannot pay all the bills, and then they are leaning on more and more debt to stay afloat.

What Is the Debt-to-GDP Ratio and Why Does It Matter?

One important question to address is, how did this couple get approved for such a large mortgage?

Well, they probably earn a decent amount since mortgage underwriters will use a debt-to-income ratio to determine an estimated amount for how much they can afford. This is similar to the nation's Debt-to-GDP ratio.

It is a comparison of how much debt the country has to how much the country is producing. A higher producing country should be able to carry more debt since they are likely economically stronger.

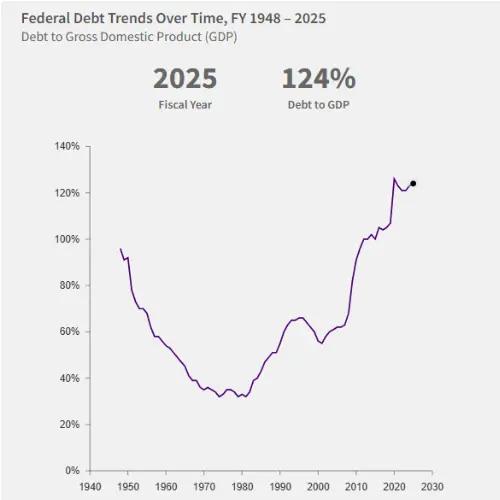

This graphic posted by fiscaldata.treasury.gov shows how quickly the nation's Debt-to-GDP has been increasing as we have been taking on more debt. Since about 2012, the US has had more debt than the economic output of the country.

This certainly highlights how the US has struggled to stick to a budget!

However, the silver lining is that we are not in the worst shape. According to World Economics, Japan and Singapore have a worse Debt-to-GDP ratio than the US. Being in 3rd on this list is not great, but at least we are not in first!

Also, it is important to note that we believe US is considered one of the economic powerhouses of the world, so that is why we are continuing to operate in this fashion.

What Are the Real Concerns for Investors?

It is very unlikely, but would be extremely concerning if the US had to declare bankruptcy and default on our loans. Our main concern revolves around the cost of the current outstanding debt.

Interest rates have been somewhat higher over the past few years and as these bonds come due, the government would greatly prefer if they could re-issue them at a lower interest rate. If the cost of the debt was cheaper then we could afford a larger debt balance.

We believe lower interest rates has been a goal for President Trump for his second term, because he understands how costly the existing debt is and we believe this is why he has been vocal about urging the Federal Reserve to lower rates. And if we can lower the interest payments, through what would effectively be a refinance, then we could potentially free up some of the government's budget.

This extra cash flow might be able to be used to start paying down some debt, or it can be used to accomplish or fund another government's goal, similar to how we allocate a client's cash flow.

Key Takeaways

- The US national debt has reached $39 Trillion, with a debt-to-GDP ratio of 124%—meaning the country owes more than its entire economic output.

- Like a household relying on credit cards to pay monthly bills, the US government operates at a deficit and continues to accumulate debt.

- The main investor concern isn't default risk, but the cost of servicing the debt—lower interest rates could effectively "refinance" the debt and free up government budget.

- While the US ranks third globally in debt-to-GDP ratio (behind Japan and Singapore), its status as an economic powerhouse allows it to continue operating with this level of debt.

Questions About Economic Policy and Your Portfolio?

If you have any questions about retirement, your individual investment portfolio, our 401(k)-recommendation service, or anything else in general, please give our office a call at (586) 226-2100.

Please feel free to forward this commentary to a friend, family member, or co-worker. If you have had any changes to your income, job, family, health insurance, risk tolerance, or your overall financial situation, please give us a call so we can discuss it.

We hope you learned something today. If you have any feedback or suggestions, we would love to hear them.

Best Regards,

Zachary A. Bachner, CFP®

with contributions by Robert L. Wink, Kenneth R. Wink, James D. Wink, and James C. Baldwin

Zach Bachner

After graduating from Central Michigan University in 2017 with specialized degrees in Finance and Personal Financial Planning, Zachary “Zach” Bachner set himself apart by earning the CFP® designation and passing the Series 7, 63, 65 licensing exams early in his career. Zach gained valuable real-world experience with the team at Summit Financial Consulting, who treated him like family. Their guidance helped him refine his skills in practical, client-centered planning, where putting their needs first was non-negotiable. This focus on trust-building not only allowed him to cultivate strong relationships, but also allowed him to continue doing what he loves most: solving client problems through efficient financial planning strategies. Leveraging his experience, Zach now helps others navigate finances through clear, informative writing. His work has been published in major outlets like Yahoo Finance, MarketWatch, and Investment Business Daily, establishing him as a valued resource. By simplifying complex topics, Zach aims to empower everyday people to confidently pursue their financial goals